{kind=link}

The

report,

detailing

the

performance

of

the

country’s

12

direct

life

assurers,

shows

the

industry

is

dominated

by

a

few

key

products

and

players,

raising

concerns

about

market

concentration

and

consumer

protection.

Direct

life

insurers

generated

total

insurance

revenue

of

ZWG4.59

billion,

approximately

US$172.05

million,

a

39

percent

increase

from

the

US$123.77

million

recorded

in

the

same

period

in

2024.

However,

this

revenue

is

heavily

concentrated.

Foreign

currency-denominated

revenue

accounted

for

55

percent

of

total

insurance

income,

down

seven

percent

from

the

previous

period’s

62

percent,

mainly

due

to

exchange

rate

stability.

“Heritage

Life

and

Nhaka

Life

failed

to

submit

their

mandatory

foreign

currency

reports.

The

Commission

urges

industry

players

to

submit

all

required

reports

on

time

to

avoid

regulatory

sanctions.”

Funeral

assurance

and

group

life

assurance

continued

to

be

the

primary

sources

of

income

for

the

life

insurance

sector,

together

accounting

for

82

percent

of

the

total

revenue.

The

share

of

revenue

generated

from

funeral

assurance

and

group

life

assurance

is

steadily

rising,

affecting

the

market

share

of

traditional

life

assurance

products.

IPEC

noted

that

a

“notable

trend

in

the

life

insurance

industry

is

the

shift

from

traditional

long

term

products

towards

predominantly

renewable

annual

policies.”

This

change

is

especially

clear

in

funeral

assurance

and

group

life

assurance

policies

currently

available.

This

practice

raises

regulatory

concerns

about

its

compliance

with

the

Funeral

Directive’s

objectives,

particularly

regarding

the

level

of

policyholder

protection,”

read

the

report.

As

a

result,

the

industry

is

strongly

encouraged

to

strictly

follow

the

rules

set

out

in

the

Funeral

Directive.

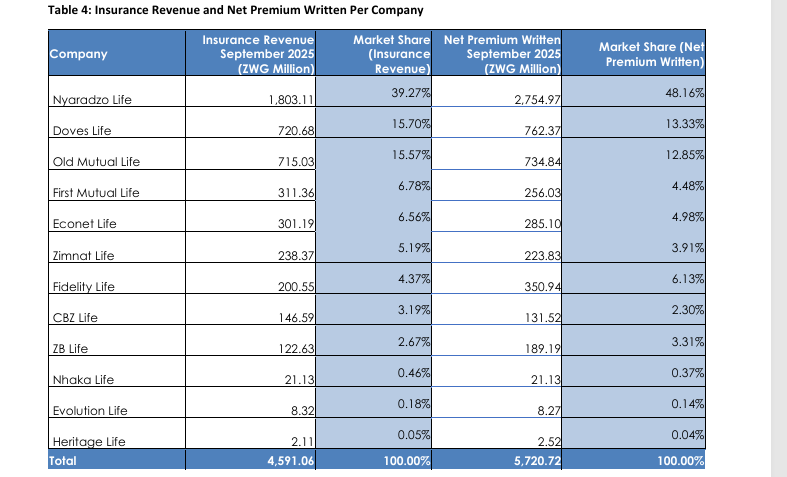

“Nyaradzo

Life

Assurance

Company

holds

the

leading

position

in

the

life

assurance

sector

with

a

39.27

percent

market

share,

largely

driven

by

its

predominant

revenue

from

funeral

assurance

policies,”

the

report

states.

The

total

revenue

of

the

top

five

companies

in

the

sector

reached

ZWG3.85

billion,

equivalent

to

US$144.33

million.

These

top

five

companies

collectively

account

for

84

percent

of

the

sector’s

total

revenue,

indicating

a

“moderately

concentrated

market.”

The

sector’s

product

mix

remains

narrow,

with

traditional

long-term

products

losing

ground.

“Funeral

assurance

remains

the

main

driver

of

the

life

assurance

sector,

representing

68.04

percent

of

total

revenue.

Group

life

assurance

is

the

second-largest

segment,

making

up

14.27

percent

of

total

revenue,”

the

report

notes.

This

concentration

raises

regulatory

concerns,

with

IPEC

highlighting

“a

notable

trend

in

the

life

insurance

industry

is

the

shift

from

traditional

long-term

products

towards

predominantly

renewable

annual

policies.

“This

change

is

especially

clear

in

funeral

assurance

and

group

life

assurance

policies

currently

available.

This

practice

raises

regulatory

concerns

about

its

compliance

with

the

Funeral

Directive’s

objectives,

particularly

regarding

the

level

of

policyholder

protection.”

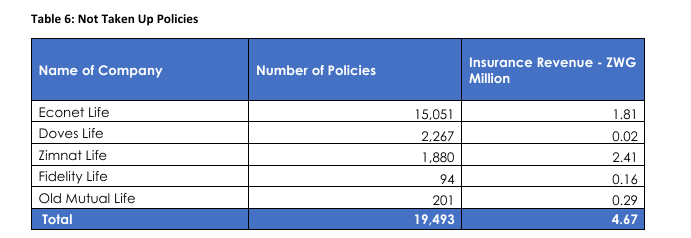

A

significant

concern

for

the

regulator

is

the

high

number

of

policies

that

are

sold

but

ultimately

not

activated

by

customers.

During

the

quarter,

the

sector

reported

19,493

Not

Taken

Up

(NTU)

policies,

leading

to

a

loss

of

projected

revenue

of

ZWG4.67

million.

The

report

singles

out

specific

companies

for

scrutiny

–

Econet

Life,

Doves

Life,

and

Zimnat

Life,

Fidelity

Life

and

Old

Mutual

Life,

which

are

strongly

advised

to

promptly

initiate

an

investigation

into

the

underlying

causes

of

their

high

NTU

rates.

“This

may

include

conducting

surveys

to

identify

specific

issues

such

as

affordability,

poor

product

understanding,

or

dissatisfaction

with

the

onboarding

process.”

IPEC

further

warns

that

“life

assurers

are

encouraged

to

closely

monitor

how

agents

present

their

products

to

potential

clients

to

prevent

misrepresentation.”

The

sector

also

continues

to

struggle

with

policies

lapsing

after

sale.

It

started

the

third

quarter

with

2

122

824

active

policies,

of

which

97

111

lapsed,

resulting

in

a

lapse

ratio

of

4.57

percent.

“Policy

lapses

are

mainly

attributed

to

affordability

issues

and

changes

in

policyholders’

circumstances,”

the

report

finds.

It

urges

insurers

to

maintain

“proactive

and

effective

communication

with

policyholders

before

lapses.”

One

company,

Nhaka

Life,

reported

an

alarmingly

high

lapse

ratio

of

27.59

percent.

“It

is

strongly

recommended

that

Nhaka

Life

conduct

detailed

experience

analyses

to

identify

the

main

reasons

for

these

elevated

lapse

rates,”

IPEC

advises,

urging

the

company

to

“craft

and

execute

targeted,

data-driven

strategies

to

lower

lapse

rates

and

enhance

policyholder

retention.”

The

report

concludes

that

the

sector’s

over-reliance

on

funeral

assurance

is

unsustainable

for

long-term

growth,

calling

for

strategic

innovation

and

diversification

to

rebuild

public

trust

and

ensure

the

industry’s

future

relevance.

Post

published

in:

Business