courtesy

of

AffiniPay.

Managing

client

funds

is

one

of

the

most

critical

responsibilities

a

law

firm

faces.

Mismanaging

trust

accounts

can

lead

to

ethics

violations,

financial

penalties,

or

even

disbarment.

That’s

why

a

thorough

understanding

of

trust

accounting

and

the

implementation

of

three-way

reconciliation

practices

are

non-negotiable.

In

this

post,

we’ll

walk

through

the

essential

three-way

reconciliation

process

and

explore

how

modern

legal

software

helps

law

firms

stay

compliant,

efficient,

and

audit-ready.

What

Is

Trust

Accounting?

Trust

accounting

refers

to

the

proper

management

of

funds

held

in

trust

on

behalf

of

a

client.

This

typically

occurs

when

a

law

firm

receives

an

advance

retainer

or

settlement

funds

that

don’t

yet

belong

to

the

firm.

These

funds

are

placed

into

a

separate

client

trust

account—often

referred

to

as

an

IOLTA

(Interest

on

Lawyers’

Trust

Accounts)

account.

The

cardinal

rule

of

trust

accounting

is

simple:

no

commingling.

Client

trust

funds

must

always

be

kept

separate

from

the

firm’s

operating

funds.

Any

earned

fees,

expense

reimbursements,

or

withdrawals

must

be

meticulously

documented

and

only

made

when

properly

invoiced

or

authorized.

To

ensure

compliance,

firms

are

expected

to

maintain

detailed

records

for

every

transaction,

including:

-

The

amount

received -

The

client

associated

with

the

funds -

The

purpose

of

the

deposit -

The

dates

and

details

of

any

disbursements

Legal-specific

accounting

software

simplifies

this

process

by

automatically

categorizing

transactions

and

assigning

them

to

individual

client

ledgers.

Why

Trust

Accounting

Matters

The

stakes

for

getting

trust

accounting

wrong

are

high.

Many

state

bars

conduct

random

audits,

and

any

discrepancies

can

result

in

disciplinary

action.

According

to

the

2025

Legal

Industry

Report,

49%

of

firms

cite

trust

accounting

as

a

moderate

or

significant

challenge,

and

61%

report

challenges

with

accounting

overall.

The

complexity

and

compliance

burden

are

real,

especially

for

small

or

solo

practices

juggling

multiple

responsibilities.

The

good

news?

With

the

right

processes

and

tools

in

place,

firms

can

turn

trust

accounting

into

a

strength

rather

than

a

liability.

Three-Way

Reconciliation:

A

Monthly

Must

One

of

the

most

effective

ways

to

maintain

accurate

trust

accounting

is

through

three-way

reconciliation.

This

practice

ensures

the

law

firm’s

trust

records

are

accurate

and

aligned

with

actual

bank

balances.

It

involves

cross-checking

three

key

elements:

-

Trust

Account

Bank

Statement:

What

your

financial

institution

reports -

Firm

Trust

Ledger:

The

internal

accounting

record

of

all

trust

activity -

Client

Trust

Ledger:

Sub-ledgers

showing

individual

client

balances

The

total

of

all

client

sub-ledgers

should

exactly

match

both

the

firm’s

trust

ledger

and

the

adjusted

bank

balance.

Any

discrepancies,

such

as

outstanding

checks

or

bank

fees,

must

be

identified

and

documented.

The

process

should

be

conducted

monthly,

though

some

jurisdictions

allow

quarterly

reconciliation.

It

should

also

be

accompanied

by

clear

documentation

and

sign-offs

to

satisfy

audit

requirements.

How

Software

Simplifies

Reconciliation

Traditionally,

three-way

reconciliation

was

handled

using

spreadsheets

and

manual

calculations,

a

process

that

is

both

time-consuming

and

error-prone.

Today,

legal

accounting

software

like

MyCase

can

automate

much

of

this

work.

With

MyCase

Accounting,

firms

benefit

from:

-

Auto-matched

transactions

to

the

trust

bank

feed -

Real-time

client

and

matter

balances -

Integrated

trust

payment

workflows -

Instant

reconciliation

reports

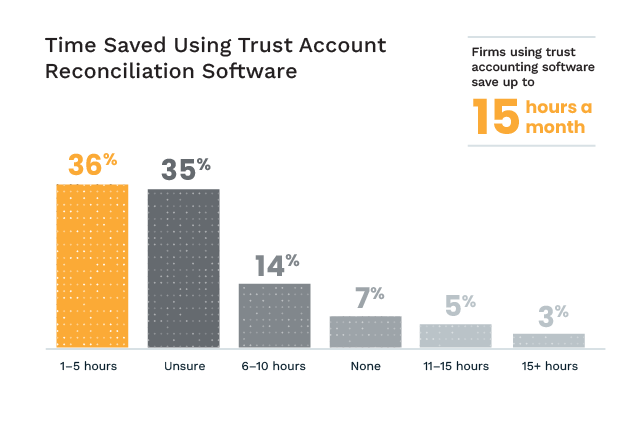

Data

from

the

2025

Legal

Industry

Report

found

that

firms

using

trust

accounting

software

save

up

to

15

hours

per

month.

Specifically,

36%

reported

saving

1

to

5

hours

monthly,

and

14%

saved

6

to

10

hours—a

powerful

endorsement

for

digital

tools

that

reduce

manual

entry

and

improve

compliance.

Best

Practices

for

Trust

Accounting

&

Reconciliation

To

ensure

your

firm

is

compliant

and

efficient,

follow

these

key

trust

accounting

best

practices:

-

Separate

Accounts:

Use

distinct

accounts

for

client

funds

and

operating

expenses.

For

large

or

long-term

matters,

consider

opening

separate

trust

accounts. -

Document

Everything:

Always

include

a

memo

or

reference

for

each

deposit

or

withdrawal.

Save

receipts,

client

instructions,

and

invoices. -

Reconcile

Monthly:

Even

if

not

required

in

your

jurisdiction,

monthly

reconciliation

is

a

best

practice

that

ensures

no

errors

go

unchecked. -

Avoid

Bank

Fees:

Ensure

your

trust

account

agreement

does

not

specify

service

charges,

overdrafts,

or

bounced

check

fees. -

Assign

Responsibility:

Delegate

trust

reconciliation

to

a

specific

person

(or

team),

and

require

dual

review

for

added

oversight. -

Use

Legal-Specific

Software:

Platforms

like

MyCase

help

reduce

human

error,

streamline

workflows,

and

automatically

track

compliance

tasks.

Streamlining

Trust

Management

With

MyCase

Trust

accounting

can

feel

intimidating,

but

it

doesn’t

have

to

be.

By

understanding

the

basics,

embracing

three-way

reconciliation,

and

using

the

right

tools,

firms

can

build

trust

with

clients

and

regulators

alike.

With

software

like

MyCase,

your

firm

can

streamline

compliance,

reduce

risk,

and

save

hours

every

month,

so

you

can

focus

on

what

matters

most:

practicing

law.

Want

to

see

how

you

can

transform

your

trust

accounting

with

MyCase?

Schedule

a

demo

today.