I’m

Nicolas,

COO

at

Juno

and

a

proud

(if

battle-scarred)

grad-school

alum

who

once

signed

on

the

dotted

line

for

nearly

$200,000

in

student

debt.

Living

through

that

experience—and

later

helping

thousands

of

classmates

do

the

same—showed

me

just

how

lopsided

the

loan

market

can

be

for

individual

borrowers.

That’s

why

Juno

was

born:

we

band

students

together,

use

their

collective

buying

power,

and

negotiate

bulk

discounts

on

private-loan

rates

and

perks

that

no

borrower

could

secure

alone.

After

several

years

of

securing

the

best

private

loan

deals

for

students

at

top

MBA

programs,

we

now

bring

the

same

no-cost

leverage

to

law

students.

Below

is

the

playbook

I

wish

someone

had

handed

me

before

orientation

day—a

step-by-step

recipe

for

keeping

your

J.D.

affordable.

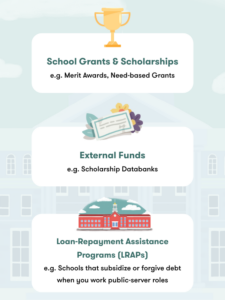

Step

1.

Chase

the

Money

You

Never

Repay

School

grants

&

scholarships

Most

law-school

“free

money”

arrives

with

your

admit

letter:

-

Merit

awards

–

driven

by

LSAT

/

GPA,

leadership

résumé,

diversity

fellowships

(e.g.,

ABA

Legal

Opportunity,

AccessLex

MAX),

or

practice-area

tracks

such

as

IP

or

public

interest. -

Need-based

grants

–

at

a

growing

list

of

schools

(Harvard,

Stanford,

Yale,

Berkeley,

Georgetown,

NYU).

External

funds

Check

the

AccessLex

Scholarship

Databank,

state-bar

foundations,

and

affinity-bar

associations

(HNBA,

NAPABA,

NBLSA,

etc.)—many

awards

have

deadlines

as

late

as

July—worth

a

final

sweep.

Loan-Repayment

Assistance

Programs

(LRAPs)

~60

ABA-accredited

schools

may

subsidize

or

forgive

part

of

your

debt

if

you

enter

public-service

or

government

roles.

Run

the

math:

LRAP

+

PSLF

can

slash

your

effective

borrowing

cost.

Step

2.

Decide

How

Much

Cash

to

Use

-

Budget

honestly.

Rely

on

your

law

school’s

published

Cost

of

Attendance

(COA),

but

note

that

summer

housing,

clinics,

moot-court

travel,

and

the

3L

bar-study

gap

often

push

actual

spending

above

that

amount. -

Keep

an

emergency

fund—include

bar-exam

and

bar-review

costs

(typically

~$3–$4k). -

Compare

returns

vs.

borrowing

cost.

Consider

your

opportunity

cost

(e.g.,

potential

investment

gains,

emergency

savings)

against

the

interest

rate

on

your

loans.

If

you

can’t

reliably

out-earn

that

rate,

using

some

savings

may

make

sense.

That

said,

many

graduates

from

T14

schools

begin

their

careers

in

Big

Law,

where

higher

starting

salaries

can

accelerate

loan

repayment

or

qualify

for

refinancing

later

on.

If

that

path

is

likely

for

you,

it

may

justify

holding

onto

more

cash

upfront

and

using

it

for

longer-term

investments.

Step

3.

Know

Your

Loan

Options

After

finishing

exploring

all

the

scholarship

options,

and

assessing

how

much

of

your

savings

you

are

willing/able

to

use,

Student

loans

are

used

to

fill

the

gap.

U.S.

citizens

and

Permanent

Residents

have

access

to

Federal

Loans.

There

are

two

types

for

Law

students:

Direct

Unsubsidized

(more

affordable

but

limited

to

$20.5k

a

year)

and

Grad

PLUS

(more

expensive,

but

can

go

up

to

the

cost

of

attendance)

Those

have

fixed

terms,

independent

of

your

specific

credit

profile.

The

terms

are

as

follows

for

the

academic

year

2025

–

2026

Key

points

-

Federal

loans

carry

IDR

plans

and

PSLF

eligibility—

most

valuable

if

you’ll

stay

in

public

service. -

Grad

PLUS

fees

add

4.228

%

to

your

balance

on

day

one

If

you

are

not

planning

to

take

advantage

of

the

Federal

protections,

it’s

worth

comparing

whether

you

can

get

a

more

affordable

loan

on

the

private

side.

Step

4.

Check

Your

Rates

on

Juno

(without

impacting

your

credit)

We

created

Juno

to

make

it

a

no-brainer

option

if

you

decide

to

take

a

private

loan.

We

negotiate

to

ensure

our

deals

are

better

than

going

directly

to

the

lender,

and

some

of

our

deals

don’t

need

a

cosigner

or

income

for

you

to

qualify.

-

Soft-credit

check

in

~2

minutes

(Does

not

affect

your

credit) -

Fixed

and

variable

APRs

that

beat

Federal

options

for

many

credit

tiers. -

Negotiated

Rates

and/or

Cash

Bonuses

are

available -

Rate

Match

Program:

If

you

find

a

better

rate

from

a

long

list

of

competitors,

we

will

match

it

and

give

you

1%

of

your

loan

amount

as

cash

back

Compare

your

personalized

Juno

quote

against

your

Federal

offers.

Step

5.

Bottom-Line

Playbook

-

Maximize

scholarships

&

LRAP

first.

Every

free

dollar

is

one

you

never

repay. -

Model

total

cost.

Include

origination

fees,

bar-prep

expenses,

and

how

quickly

you’ll

refinance

or

pursue

PSLF. -

Shop

with

soft

checks.

Gather

real

quotes,

then

decide—without

any

impact

on

your

credit. -

Decide

what

combination

of

Federal

and

Private

loans

you

are

going

to

use:

You

can

use

any

combination

of

Federal

and

Private

loans

up

to

your

COA. -

Move

early.

If

you

see

a

rate

you

like,

consider

applying

early

to

lock

it

in.

Remember,

rates

may

move

at

a

moment’s

notice.

Law

school

is

a

major

investment,

but

thoughtful

planning

can

keep

your

debt

in

check

so

you

can

focus

on

contracts,

criminal,

or

con-law

instead

of

compounding

interest.

Juno

helps

law

students

access

discounted

deals

through

collective

bargaining,

so

you

can

borrow

smarter

and

stress

less.

Best

of

luck

in

your

legal

journey!

The

information

provided

in

this

article

is

current

as

of

June

4,

2025,

and

is

intended

for

general

informational

purposes

only.

It

does

not

constitute

legal,

financial,

or

tax

advice.

Readers

should

consult

their

own

advisors

before

making

any

decisions.

Terms

and

conditions

may

apply

to

the

loan

products

discussed.

Federal

student

loans

offer

certain

borrower

protections

and

benefits—such

as

income-driven

repayment

plans

and

potential

forgiveness

options—that

may

be

important

to

consider.

To

learn

more,

visit

studentaid.gov.