Images

Editor’s

note:

Second

in

a

three-part

series.

Read

the

first

installment

here.

You’ve

gathered

reliable

company

data.

You’ve

determined

the

law

department’s

proper

lane

for

this

transaction.

You’ve

maintained

appropriate

confidentiality

and

applied

sound

organizational

principles.

Now,

the

ink

is

dry

on

your

merger

agreements

—

and

your

GC

is

facing

down

a

new

challenge:

guiding

the

integration

of

a

portfolio

of

companies

into

an

existing

structure.

“Every

company

has

different

internal

dynamics

and

different

ways

of

working,

right?”

says

Kariem

Abdellatif,

the

head

of

Mercator

by

Citco

(Mercator),

a

specialist

entity

management

provider

that

helps

organizations

manage

their

global

entity

portfolios,

including

during

complex

M&A

transactions.

“So

the

system

you

set

up

has

to

be

able

to

accommodate

those

differences,

and

the

entire

governance

framework

for

managing

entities

needs

to

be

flexible

enough

to

handle

not

just

the

current

complexity,

but

also

future

organizational

changes.”

In

this

series,

we’re

providing

a

step-by-step

guide

for

general

counsel

navigating

a

merger

or

other

corporate

transaction.

In

part

one,

we

explored

best

practices

for

corporate

law

departments

in

the

pre-merger

phase.

Here,

we’re

sharing

the

initial

to-do

list

for

a

law

department

once

a

transaction

is

closed.

We’ll

also

be

discussing

these

topics

in

a

webinar

next

month.

You

can

pre-register

here.

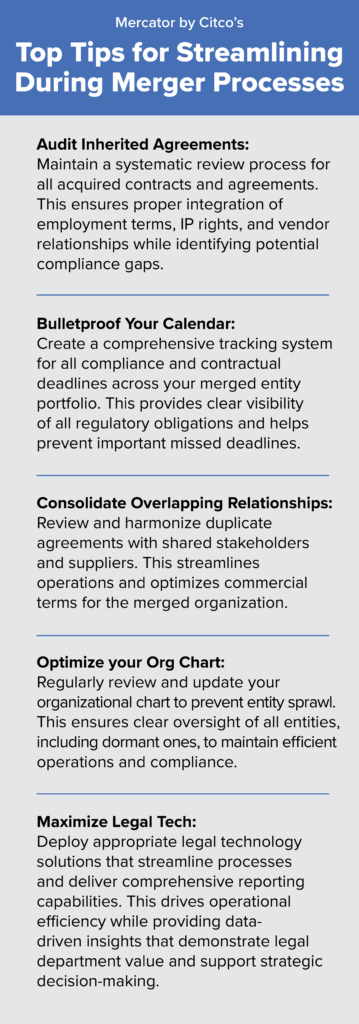

Button

Up

Your

Contracts

Law

departments

would

be

well-advised

to

get

a

head

start

on

shoring

up

their

employment

and

intellectual

property

agreements

as

soon

as

a

deal

is

inked.

This

is

particularly

so

when

a

large

company

buys

a

smaller

entity

in

an

equity

deal,

notes

Scott

Naturman,

an

M&A

partner

with

Hughes

Hubbard

&

Reed

LLP.

That’s

because

smaller

companies

often

have

deficient

regulatory

and

internal

compliance

programs,

which

can

lead

to

contracting

problems.

“Almost

every

deal

we

do,

we

find

deficiencies,

and

it’s

not

me

necessarily,

but

it’ll

be

my

HR

and

IP

colleagues

looking

at

employment-related

contracts

and

finding

deficiencies

in

them,”

Naturman

says.

“So

that’s

something

that

often

has

to

be

fixed.”

Problems

can

also

arise

related

to

the

merged

entity’s

commercial

contracts.

Mergers

often

occur

between

companies

in

similar

industries,

of

course.

As

a

result,

the

merged

entity

may

have

contracts

with

the

same

customers

and

suppliers

as

the

acquirer.

If

multiple

contracts

with

the

same

customer

or

supplier

have

differing

terms,

Naturman

notes,

the

merged

business

will

look

to

maintain

the

best

possible

outcome

while

combining

the

contracts.

Some

items

like

“most

favored

nation”

clauses

will

often

be

vetted

and

mitigated

in

the

due

diligence

process,

but

lawyers

will

still

need

to

think

through

how

to

merge

any

overlapping

agreements

once

the

deal

is

closed.

Maximize

the

Interim

Period

Even

if

they

tend

to

be

billed

as

“mergers

of

equals,”

few

mergers

are

actually

created

equal.

One

key

difference

emerges

around

the

closing

structure

—

with

delayed

and

simultaneous

closings

presenting

their

own

challenges

and

opportunities.

When

there’s

a

delayed

closing,

law

departments

must

navigate

an

interim

period,

where

you

protect

the

value

of

the

business

while

awaiting

a

condition

to

be

met

—

regulatory

approval,

for

example,

or

the

greenlight

from

a

lender.

Naturman

notes

that

law

departments

can

make

progress

on

essential

human

resources

and

intellectual

property

tasks

during

this

period.

“You

want

the

in-house

folks

as

soon

as

possible

to

be

speaking

with

key

employees

and

trying

to

lock

them

into

agreements

on

their

own

paper,

but

you

can’t

have

anything

become

effective

until

the

deal

closes,

of

course,”

he

says.

“If

you

have

a

delayed

closing,

you

can

reach

a

wider

audience,

while

if

it’s

simultaneous,

you

don’t

have

that

opportunity.”

Update

—

and

Leverage

—

Your

Org

Chart

Simply

gathering

accurate

data

poses

another

post-merger

challenge

for

law

departments.

All

of

the

documents

related

to

the

acquired

company

must

be

uploaded

into

a

merged

system,

for

example,

and

they

must

be

made

available

to

the

appropriate

employees.

Once

the

information

is

updated,

Mercator’s

Entica

platform

can

create

detailed

and

interactive

corporate

org

charts.

This

allows

users

to

visualize

the

full

organization

—

which

entity

sits

on

top,

what

happens

if

entities’

locations

are

moved,

what

it

would

mean

if

an

entity

were

liquidated.

Law

departments

at

this

stage

should

consider

their

portfolio

of

companies,

looking

for

entities

that

could

be

merged.

Some

may

see

an

opportunity

for

immediate

savings.

“If

you

have

two

of

your

own

entities

in,

say,

France,

and

you

just

acquired

a

portfolio

that

has

three

other

entities

in

France,

there’s

a

case

for

rationalization,”

Mercator’s

Abdellatif

says.

“Ask

yourself:

‘Why

do

I

have

five

entities

in

France?

Do

I

actually

need

all

of

these

for

the

activities

I

perform,

and

what

are

the

cost

and

compliance

implications

of

maintaining

them?”

When

companies

neglect

their

org

chart,

it

can

also

create

long-term

problems,

according

to

Naturman.

“Especially

if

you’re

a

serial

buyer

and

you’re

buying

companies,

you

may

end

up

having

a

web

of

entities,

and

it

just

gets

out

of

control

and

hard

to

manage,”

he

says.

This

type

of

sprawl

can

create

tax

inefficiencies

and

prevent

organizations

from

minimizing

liabilities

by

housing

them

in

carefully

chosen

entities

within

the

organization’s

structure.

“I

don’t

think

enough

of

that

planning

happens,”

Naturman

says.

“It’s

often

we’re

brought

in

five

years

later

to

help,

then

they

say:

‘Help

us.

It’s

a

complete

mess.

How

do

we

reorganize

ourselves?

How

do

we

get

this

under

control?’”

Mercator’s

Abdellatif

adds:

“Dormant

entities

often

become

problematic

when

overlooked

during

transitions

or

treated

as

‘out

of

sight,

out

of

mind.’

We

frequently

see

cases

where

incomplete

records

or

unclear

responsibilities

lead

to

surprise

liabilities.”

“The

solution

is

treating

dormant

entities

with

the

same

discipline

as

active

ones,”

he

says,

“maintaining

accurate

inventories,

assigning

clear

ownership,

conducting

regular

reviews,

and

ensuring

professional

oversight.

This

transforms

them

from

hidden

risks

into

manageable

assets.”

Create

an

Impeccable

Calendar

Onboarding

an

entity

also

means

onboarding

its

deadlines.

Once

a

transaction

is

closed,

detailed

deadline

calendaring

is

a

key

step

for

GCs.

Critically,

this

step

isn’t

limited

to

deadlines

related

to

the

deal

itself.

Staying

on

top

of

deadlines

means

understanding

when,

say,

a

customer

supplier

contract

will

expire,

Naturman

notes.

Maintaining

this

focus

is

a

key

to

successfully

merging

multiple

entities.

“One

thing

I’ve

seen

over

the

course

of

my

career

is

less

diligence

being

done,

or

more

targeted

diligence,”

he

says.

Abdellatif

notes

that

Mercator’s

Entica

system

contains

robust

workflow,

calendaring,

and

compliance

capabilities,

among

its

other

features.

Mergers

are

a

logistical

exercise,

he

says,

and

the

right

technology

can

form

the

organizational

backbone

for

a

transaction

to

progress.

“Technology

functions

differently

within

each

corporate

environment

—

meaning

it

doesn’t

always

get

used

the

same

way,”

he

says.

“To

get

the

most

value

out

of

it,

you

need

to

make

sure

that

its

properly

adapted

to

each

specific

environment.”

He

adds:

“When

implemented

thoughtfully,

technology

becomes

more

than

just

a

system

—

it

becomes

the

foundation

that

helps

standardize

processes,

maintain

compliance,

and

ultimately

drive

successful

integration.”

Stay

tuned

for

the

next

article

in

this

series,

where

we’ll

be

exploring

steps

to

consider

during

the

negotiation

and

closing

of

a

transaction. You

can

register

for

our

webinar

on

these

topics

here.